October 23, 2025

Will The Fed Rate Cut Help Housing Affordability?

Author: Ivory Innovations Director of Student Programs Keni Nelson

On September 17th, 2025, the Federal Reserve voted to cut rates for the first time that year and signaled that more cuts are on the way. This move was in response to growing concerns over the slowing labor market, and the hope is that by making borrowing cheaper, economic growth will follow and help turn the tide on employment.

While the benefit of a rate cut makes sense on a macroeconomic level, the impact of these rate cuts on everyday people is more abstract and indirect. Can this lead to housing prices going down? Will this make mortgages more affordable?

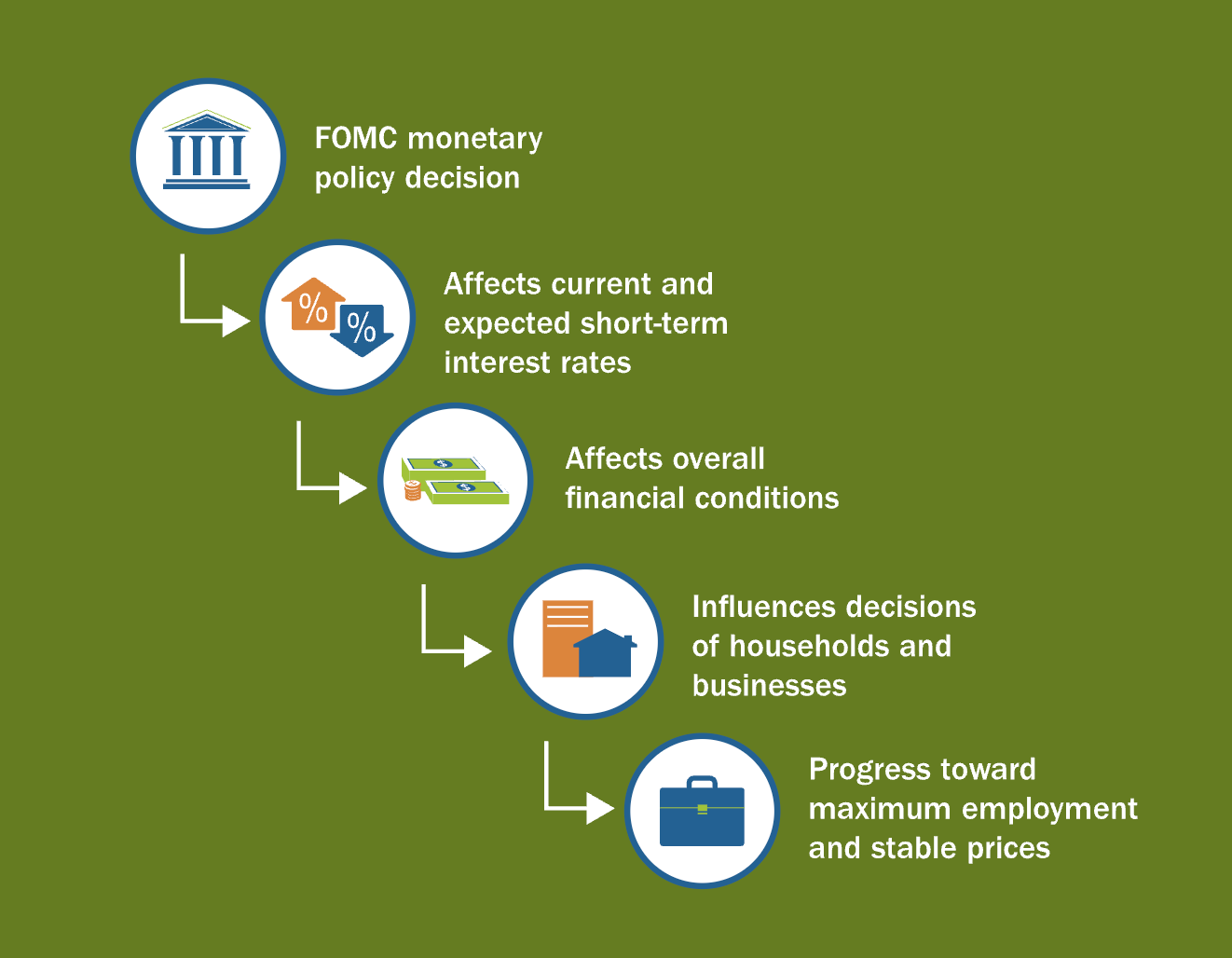

The answer is complicated. Rate cuts can have an immediate influence on parts of the housing market, but the impacts and benefits are months, and oftentimes years, down the road. Let’s talk through how a rate cut at the Federal level trickles down through the economy, and what it means for housing specifically.

Overview: The Federal Reserve

The Federal Reserve serves as the central bank for the United States. Its primary functions are to “maximize employment, stabilize prices, and moderate long-term interest rates”. How this is done is very nuanced and detailed, but in the simplest terms, they accomplish this through strategic interest rates. You raise rates to cool the economy and make sure that there’s no oversupply, you lower rates to heat the economy and make sure economic activity is growing.

Whenever the Fed is making a decision, just remember that it’s being done to “promote maximum employment and stable prices.”

(Somewhat) Immediate Benefit: Construction Loan Terms

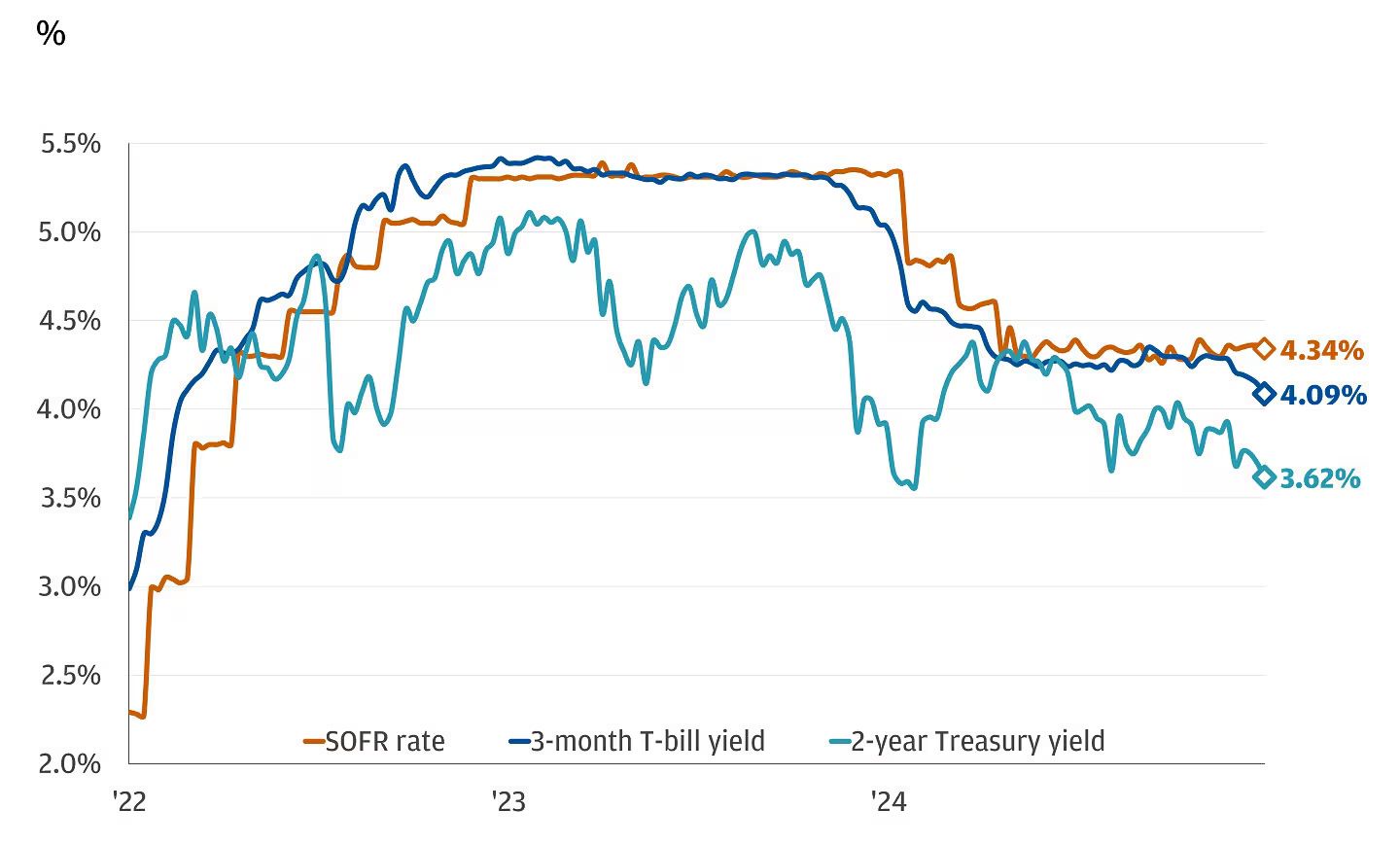

The first impact of a rate cut is felt in the Overnight Funding Markets. For most folks, this doesn’t really mean much. But for home builders, this is the first place where they can see a benefit. When a home builder needs to get a construction loan, the interest rate the bank will offer takes a few factors into consideration. The biggest variable is the Secured Overnight Financing Rate (SOFR).

Banks are required to have a certain amount of cash on hand to make sure that they have the necessary funds to settle any outstanding payments. Depending on the day's lending activities, a bank may not have enough cash, so the Fed will supply the necessary funds to ensure the bank complies. But the Fed doesn’t do this out of the goodness of its heart; there is a cost to the bank for this cash. That cost is the SOFR. And the SOFR is directly tied to the Federal Interest Rate.

SOFR + Spread = Construction Loan Interest Rate

The spread is variable and based on the discretion of the bank, but is typically an additional 1-2% interest.

When the Fed cuts interest rates, it means that home builders can borrow money more cheaply, which can translate down the line to a cheaper final product, AKA, a home at a lower price point.

Improved Treasury Market = Improved Mortgage Environment

Most banks don’t service the mortgages they issue. Most are sold to various institutions, where they’re bundled into mortgage-backed securities (MBS) and sold to investors. You may read that sentence and feel the presence of the Ghost of Recessions Past, but much has changed since the 2008 Financial Crisis, where the MBS market cratered the economy and housing prices. The flow of funds from the lender to the secondary market, and then to investors, is critical to keeping the housing market active and allows lenders to continue to deploy capital.

As with any investment, there’s always risk. When you invest in an individual stock, your risk is higher since everything rides on the company being successful and hitting its benchmarks. You’ve literally put all your eggs in one basket. That is why most financial advice says to invest in funds, where several stocks are all pooled together, and your risk is more diversified.

With mortgage-backed securities, you’re thinking about risk the same way an investor would look at a fund. Yes, one homeowner may default on their mortgage, but since there are thousands of mortgages in an MBS, the individual investor's risk is balanced by all the other mortgages being paid on time.

But how do you get an investor to pick an MBS over another kind of fund? How do we ensure that there are enough investors interested in this financial product to make sure that lenders have funds to give to future home buyers?

This is where the relationship between the federal interest rate and MBS comes into play. This junction happens at the U.S. Department of the Treasury.

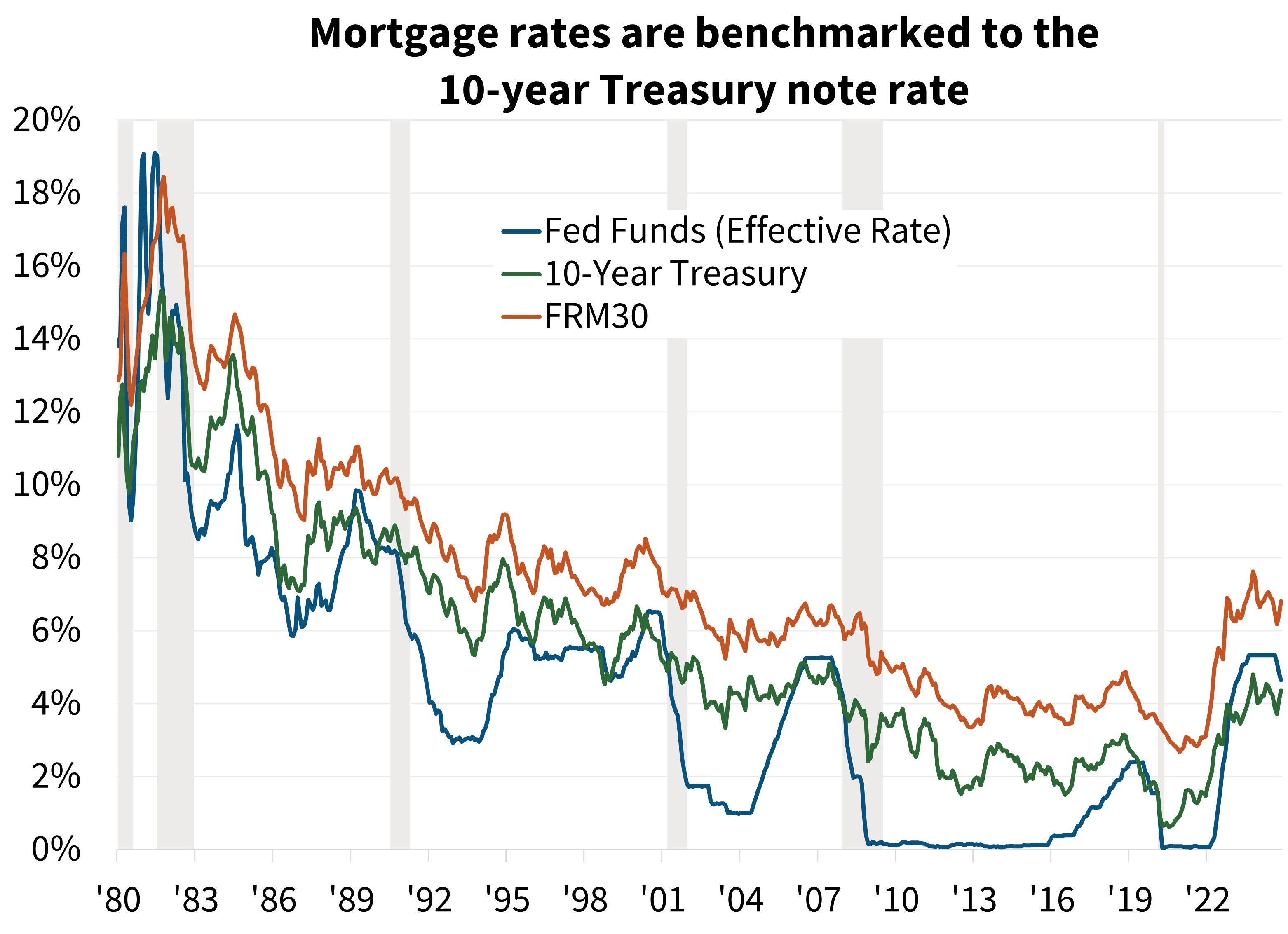

The U.S. Department of the Treasury is responsible for managing all federal finances. And while the federal government brings in trillions of dollars annually through taxes, spending often outpaces revenue. To help ensure that government operations and projects continue uninterrupted, the Treasury issues various investment opportunities to bring in liquidity. These come in many different forms, but we’ll focus on something called the 10-year Treasury Note, or 10-year T-Note.

A 10-year T-Note is, in the simplest terms, a loan that investors give to the federal government, which will be paid back in 10 years. The amount of money investors make is based on the interest rate charged on the note. And guess who determines the interest rate? The Federal Reserve. This is one of the safest investments a person can make, because the likelihood of the United States Federal Government not being able to pay back the loan is, for our purposes, nonexistent.

While a mortgage may be for 30 years, most homeowners only own their home for 7-10 years. Most MBS aggregators consider this and set an “expected life” of 5-10 years. Conveniently, that is the same maturity timeline of a 10-year T-Note.

Because the expected life of most mortgages and the maturity of the 10-year T-Note line up so closely, the 10-year has become the benchmark that financial markets use to price mortgage-backed securities. Investors don’t compare MBS to a stock fund or even a short-term Treasury bill, they compare them to the yield they could get from a 10-year T-Note, which is considered essentially risk-free. To make an MBS attractive, it must offer a higher yield than the 10-year, and that difference is called the spread.

When the Federal Reserve lowers interest rates, yields on Treasuries, including the 10-year, tend to fall. As those yields decline, the benchmark against which MBS are priced also moves lower. This means the spread can still compensate investors for the additional risk, while the absolute level of mortgage rates available to consumers comes down. In other words, the cost of borrowing for homebuyers decreases, not because the Fed sets mortgage rates directly, but because its policies ripple through the Treasury market, into MBS pricing, and finally into the rates offered by lenders.

The Bottom Line

The relationship between federal interest rates and housing affordability is, to say the least, complicated. A cut by the Fed works its way through overnight lending markets like SOFR, easing the cost of construction loans. Then, through Treasuries, which sets the benchmark for MBS pricing, and ultimately into the mortgage rates offered to homebuyers.

But interest rates are only one piece of the housing affordability puzzle. Affordability also depends on supply constraints, material costs, availability of labor, zoning and regulatory policies, and the broader health of the economy. Rate cuts make borrowing cheaper, but it doesn’t directly solve limited inventory or rising construction costs.

While we can celebrate rate cuts and the impacts they’ll have for builders, lenders, and buyers, the impact on housing prices and affordability is gradual and won’t provide relief anytime soon.